Starting a business has never been easier. A website, a payment processor, and a social media page can be live before lunch. Anyone with a laptop and an idea can call themselves a founder by the end of the week.

Staying in business is a different story entirely.

According to the latest U.S. Bureau of Labor Statistics data, roughly one in five new businesses close within their first year. Within five years, almost half are gone. By the ten-year mark, about two-thirds have shut their doors. These aren’t scare-tactic numbers pulled from a motivational speech – they’re from the BLS Business Employment Dynamics survey, and they’ve held in a fairly consistent range for years.

I’ve spent enough years building and running businesses to know that these numbers don’t tell the whole story, though. Behind every closure is usually a string of small, fixable decisions that compounded over months or years. Founders rarely wake up one morning and decide to fail. They drift into it – one skipped financial review, one ignored customer complaint, one “we’ll fix that later” at a time.

This article isn’t here to scare you out of starting something. It’s here to do the opposite: to walk through exactly why small businesses fail, in plain language, so you can spot the warning signs in your own business before they become unrecoverable. We’ll cover the nine most common causes of failure, the early signs that something is going wrong, and the habits that separate businesses that survive from the ones that don’t.

If you’re building something right now, or thinking about it, this is the article I wish someone had handed me earlier in my own journey.

Why Do Most Small Businesses Fail?

Here’s the uncomfortable truth: failure is rarely caused by one big, dramatic mistake. There’s no single moment where a founder makes one bad call and the business collapses the next day.

It’s almost always death by a thousand small cuts.

A pricing decision that seemed fine in year one becomes unsustainable in year two. A marketing plan that worked when the founder had time to post every day quietly stops working once the business gets busier and the posting stops. A cash cushion that should have been three months thick was never built because the business was “doing fine.”

This pattern shows up consistently in research on business failure. CB Insights, which has spent over a decade analyzing startup post-mortems, updated its landmark study in 2024 using data from more than 400 venture-backed companies that shut down. The headline number – that businesses “run out of cash” – was true for roughly 70% of them. But CB Insights was explicit about something important: running out of cash is the symptom, not the disease. The real root causes were poor product-market fit (cited by 43% of failed companies), bad timing (29%), and unsustainable unit economics (19%).

In other words, the bank account didn’t hit zero because the business got unlucky. It hit zero because something upstream – usually a lack of real demand, or a cost structure that never made sense – was broken long before the cash ran out.

This article breaks down the major causes worth understanding, in the order they tend to show up in a business’s life: starting without validating demand, mismanaging cash, operating without a plan, marketing weakly, ignoring feedback, financial mismanagement, trying to do it all alone, scaling too fast, and failing to adapt. Some of these will overlap. Most businesses that fail are dealing with two or three of these at once, not just one.

Let’s go through each one.

1. Starting Without Validating the Market

The Problem

This is the single most common root cause of business failure, and it’s also the most avoidable.

Founders fall in love with their idea before they fall in love with their customer’s problem. They spend months – sometimes years – building a product, perfecting the branding, and rehearsing the pitch, all before finding out whether anyone actually wants what they’re building badly enough to pay for it.

The data on this is remarkably consistent. CB Insights’ research, going back over a decade of post-mortems, has repeatedly found that a lack of real market need is the leading cause founders themselves cite when their company shuts down. It’s not a new problem, and it’s not specific to tech startups – it shows up just as often in local service businesses, restaurants, retail shops, and agencies.

The trap is subtle. It’s easy to mistake enthusiasm from friends, family, and your own excitement for genuine market demand. People will tell you your idea is great because they like you, not because they’re going to buy it. That’s encouraging, but it’s not evidence.

How to Avoid It

Conduct real market research before you commit serious money. This doesn’t need to be a formal, expensive study. It means understanding who your competitors are, what they charge, what their customers complain about, and where the gaps are.

Talk to potential customers directly – not your inner circle. Ask open-ended questions about the problem you think you’re solving, not leading questions about your specific solution. You’re trying to find out if the pain is real and urgent, not whether people are polite enough to encourage you.

Validate demand before you invest heavily. This could mean a simple landing page that measures sign-up interest, a small batch of pre-orders, a pilot run with a handful of real paying customers, or a minimum version of your service offered to a small group before a full launch. The goal isn’t to build the perfect product. It’s to find out, as cheaply and quickly as possible, whether people will actually pay for what you’re planning to build.

If you take one thing from this section, let it be this: validation is not a delay tactic. It’s the fastest way to avoid spending a year building something nobody needs.

2. Poor Cash Flow Management

The Problem

A business can be growing, getting great reviews, and still die from cash flow problems. This catches a lot of first-time founders off guard, because it feels counterintuitive – how can a business with paying customers run out of money?

The answer lies in the difference between revenue and profit, and more specifically, the timing of money coming in versus money going out. A business might invoice a client for a large project but not get paid for sixty or ninety days, while rent, payroll, and supplier costs are due every month regardless. Revenue on paper doesn’t pay today’s bills. Cash in the bank does.

This is one of the most well-documented causes of small business failure, and the data behind it is sobering. Multiple industry studies, including research cited by SCORE and U.S. Bank, have found that cash flow problems are linked to the vast majority of small business closures – not because the businesses weren’t generating sales, but because they weren’t managing the timing and reserves around that money.

How to Avoid It

Track monthly expenses with real discipline, not just a glance at the bank balance. Know exactly where your money goes every month – fixed costs, variable costs, one-off expenses – so nothing sneaks up on you.

Maintain an emergency fund. Most financial advisors for small businesses recommend keeping at least three to six months of operating expenses in reserve. It feels excessive when things are going well. It’s the difference between surviving a slow quarter and shutting down because of one.

Monitor cash flow weekly, not just at tax time. A simple spreadsheet that tracks what’s coming in, what’s going out, and when, will surface problems while there’s still time to act. Waiting until the quarterly review to notice a cash crunch is often too late to fix it gracefully.

Cash flow management isn’t glamorous. It’s also one of the most reliable predictors of whether a business survives its first few years.

3. No Clear Business Plan

The Problem

Plenty of businesses operate day to day without a real sense of direction. They react to whatever’s urgent – a client request, a problem with a vendor, a slow week – without a framework for deciding what actually matters.

This isn’t about skipping a fancy 40-page business plan document. Most of those never get read again after the first draft. The real problem is more basic: not having clear goals, not knowing what success looks like in three months or a year, and not having a way to measure whether the business is actually moving forward or just staying busy.

Without a plan, decisions get made on gut feeling and urgency rather than priority. That works for a while. It tends to stop working once the business has more moving parts than one person can hold in their head.

How to Avoid It

Create a simple business roadmap. This can be one page. It should answer a few core questions: what are we building, who is it for, how do we make money, and what needs to be true in the next 90 days for this to be working.

Set quarterly and yearly objectives that are specific enough to measure. “Grow the business” isn’t a goal. “Increase repeat customers by 15% this quarter” is.

Review and update the plan regularly. A plan that never changes isn’t a strength – it’s usually a sign nobody’s looking at it. Markets shift, costs change, and customer needs evolve. Revisiting the plan every quarter keeps it useful instead of decorative.

A business plan isn’t a document you write once and file away. It’s a working tool you return to when you need to decide what to say yes to and what to let go.

4. Weak Marketing Strategy

The Problem

There’s a quiet assumption a lot of new business owners make: if the product or service is good enough, customers will find it. They won’t – not reliably, and not at the volume needed to sustain a business.

The market is crowded, attention is scattered across more platforms than ever, and customers have more options than at any point before. A great product with no visibility loses to an average product that’s easy to find, easy to trust, and shows up consistently where people are already looking.

This shows up constantly in small businesses that struggle: a beautiful product or service, almost no consistent way for new customers to discover it, and a founder who assumed word of mouth would be enough.

How to Avoid It

Build a strong, consistent online presence. This means a clear website or profile that explains what you do and who you do it for, kept current – not a page built once at launch and never touched again.

Invest in content marketing and SEO as long-term, compounding assets rather than one-time campaigns. Helpful content that answers real questions your customers are searching for keeps working long after it’s published, unlike a one-off ad.

Leverage social media and email marketing together, not as separate efforts. Social media is good for visibility and discovery. Email is good for staying in front of people who’ve already shown interest but haven’t bought yet. Most businesses lean entirely on one and ignore the other.

Marketing doesn’t need to be loud or expensive to work. It needs to be consistent, and it needs to be aimed at the right audience.

5. Ignoring Customer Feedback

The Problem

It’s tempting to build based on instinct – what you think customers want, what you’d want if you were the customer, what worked for a competitor you admire. The risk is building an entire product or service around assumptions that were never actually tested against real customer feedback.

This is especially dangerous for businesses past their first year. Early on, founders are usually close to their first customers and hear feedback constantly, even informally. As the business grows, that direct contact often fades, replaced by assumptions about what customers want based on outdated impressions.

How to Avoid It

Collect reviews actively, rather than hoping satisfied customers leave them unprompted. Most won’t, even if they’re genuinely happy. A simple, polite ask after a purchase or project completion goes a long way.

Run customer surveys on a regular cadence. They don’t need to be long. A few focused questions about what’s working, what’s frustrating, and what they wish existed will surface patterns you won’t see from inside the business.

Continuously improve products and services based on what you learn, rather than treating feedback as something to collect and file away. The businesses that stay relevant treat customer input as an ongoing loop, not a one-time survey they ran during launch week.

Customers will tell you what’s wrong with your business if you ask the right way and actually listen. Most failures in this category aren’t from a lack of feedback – they’re from feedback that was collected and never acted on.

6. Poor Financial Planning

The Problem

This is broader than cash flow specifically. It covers the everyday financial decisions that quietly erode a business’s stability: spending more than the business can sustain, pricing products or services without a clear sense of margin, and taking on debt without a realistic plan to pay it back.

Overspending often happens gradually – a slightly nicer office, a tool subscription that seemed worth it, a hire made a little too early. Incorrect pricing is its own trap: many small business owners price based on what competitors charge or what feels fair, without actually calculating their true costs, which means they can be “profitable” on paper while actually losing money on every sale. And debt, while sometimes necessary for growth, becomes dangerous when it’s taken on reactively, to cover a shortfall, rather than strategically.

How to Avoid It

Create a monthly budget and stick to it. This doesn’t need complex software. A clear breakdown of fixed costs, variable costs, and expected revenue, reviewed every month, catches problems before they snowball.

Track profit margins by product or service line, not just overall revenue. It’s common for a business to have one offering quietly losing money while another subsidizes it, and the owner never notices because the topline numbers look fine.

Review financial reports regularly, not just at tax season. A monthly look at profit and loss, even a simple one, keeps financial reality visible instead of something that gets discovered as a surprise.

Good financial planning isn’t about being an accountant. It’s about treating the numbers as a regular part of running the business, not an afterthought.

7. Trying to Do Everything Alone

The Problem

A lot of founders start out wearing every hat – sales, operations, marketing, customer service, bookkeeping – often because there’s no budget to hire help and no team yet to delegate to. That’s a normal and even necessary phase early on.

The problem is when it doesn’t change. Founders who keep trying to do everything themselves, well past the point where the business could support help, tend to hit two walls: burnout, and a growth ceiling that has nothing to do with market demand and everything to do with one person’s limited hours in a day.

Burnout shows up as declining decision quality, slower response times, and eventually, disengagement from a business the founder once loved. Slow growth shows up as missed opportunities – deals not followed up on, marketing that never gets consistent, customer issues that pile up because there’s no one dedicated to handling them.

How to Avoid It

Delegate tasks that don’t require the founder’s specific judgment. Not every decision needs the founder in the room. Identify the repetitive, lower-stakes work first and hand it off.

Outsource specialized work like accounting, legal review, or design rather than trying to learn these from scratch under time pressure. A few hours of a specialist’s time is often cheaper, in time and in mistakes avoided, than a founder learning it badly on the side.

Build the right team deliberately, rather than hiring reactively whenever things feel overwhelming. Think about what the business will need in six to twelve months, not just what’s urgent this week.

Trying to do everything alone feels like control. In practice, it’s usually one of the quieter reasons a business plateaus.

8. Growing Too Fast

The Problem

Growth feels like validation, so it’s tempting to chase it as fast as possible – more locations, more hires, more product lines, more customers, all at once. But growth that outpaces a business’s underlying systems is a well-documented failure pattern, particularly among high-growth businesses. Research on premature scaling has found it to be a recurring factor behind failures even at companies with strong demand and funding, because the operational foundation wasn’t ready to support the pace of expansion.

The warning signs usually show up as quality slipping, customer service response times growing, and internal processes that worked for a ten-person team breaking down at fifty.

How to Avoid It

Scale gradually, in stages, with clear checkpoints rather than one big leap. Test growth in a contained way before committing fully.

Build processes first. Before adding volume, make sure the systems – how orders get fulfilled, how customer issues get resolved, how new hires get trained – can handle more than they currently do.

Monitor operational capacity as closely as revenue. Revenue growth that outpaces the team’s ability to deliver quality is a short-term win and a long-term risk. Keep an eye on both numbers, not just the one that looks good in a pitch deck.

Fast growth isn’t inherently bad. Growth without the infrastructure to support it usually is.

9. Failure to Adapt

The Problem

Markets change. Customer expectations shift. New competitors enter. Technology – including the recent acceleration in AI-powered tools – is changing how customers research, compare, and buy from small businesses faster than most owners can comfortably track.

Businesses that succeed in year one sometimes fail in year five for one simple reason: they kept doing exactly what worked when they started, while the world around them moved on. This is a particularly easy trap to fall into once a business is stable – there’s a strong incentive to protect what’s working rather than risk changing it.

How to Avoid It

Review competitors on a regular schedule, not only when sales start slipping. Understand what they’re doing differently, not to copy them, but to know where the market is heading.

Follow industry trends consistently, even the ones that feel slightly outside your core focus. The businesses that get blindsided are usually the ones that stopped paying attention.

Embrace innovation as an ongoing habit, not a one-time pivot triggered by a crisis. Small, regular improvements are far less risky than a single dramatic change made under pressure because the business waited too long.

Adaptability isn’t about chasing every new trend. It’s about staying close enough to your market that change doesn’t catch you by surprise.

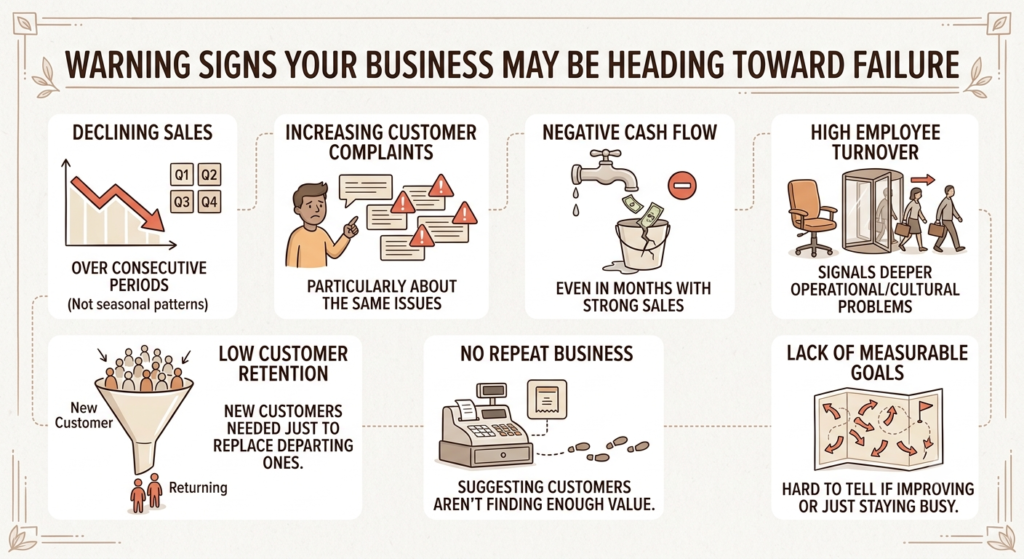

Warning Signs Your Business May Be Heading Toward Failure

Most businesses don’t fail overnight. There are usually warning signs visible months, sometimes years, in advance – if someone is paying attention. Here are the ones worth watching closely:

- Declining sales over consecutive periods, especially if it’s not explained by a known seasonal pattern

- Increasing customer complaints, particularly about the same issue repeating

- Negative cash flow, even in months with strong sales

- High employee turnover, which often signals deeper operational or cultural problems

- Low customer retention, where new customers are needed constantly just to replace the ones who leave

- No repeat business, suggesting customers aren’t finding enough value to come back

- Lack of measurable goals, making it hard to tell whether the business is actually improving or just staying busy

None of these alone means a business is doomed. But when two or three of them show up at the same time, it’s worth stopping to take a closer look rather than waiting for the next quarter to see if things improve on their own.

10 Habits of Businesses That Stay Successful

The flip side of all of this is more encouraging. Businesses that last tend to share a recognizable set of habits, regardless of industry:

- Focus on customers as the center of every major decision, not an afterthought to product or operations.

- Track business metrics consistently, so problems surface early instead of becoming crises.

- Invest in marketing as an ongoing function, not a campaign that runs only when sales slow down.

- Learn continuously – about the market, the customer, and the craft of running the business itself.

- Build strong teams, with clear roles and the trust to delegate real responsibility.

- Manage cash wisely, treating reserves and cash flow visibility as non-negotiable.

- Innovate regularly, in small increments rather than waiting for a crisis to force change.

- Deliver consistent quality, every time, not just when things are going well.

- Plan for long-term growth, balancing today’s priorities against where the business needs to be in a few years.

- Stay adaptable, treating change as a constant rather than an exception.

None of these are dramatic. That’s the point. Long-term business success tends to look boring from the outside – consistent, disciplined, unglamorous work, repeated for years.

A Simple 30-Day Business Health Check

If you’ve read this far and you’re wondering where to start, here’s a practical checklist you can run through over the next 30 days. It won’t fix everything at once, but it will tell you, honestly, where your business stands.

- Review your finances. Look at cash flow, profit margins, and outstanding debts with fresh eyes.

- Analyze your marketing performance. Which channels are actually bringing in customers, and which are just busywork?

- Talk to your customers. Reach out directly – even five real conversations will surface more than a quarter of guessing.

- Evaluate your competitors. What are they doing now that they weren’t doing a year ago?

- Check your business goals. Are they written down anywhere, and are you actually on track?

- Improve one weak area. Don’t try to fix everything at once. Pick the single most urgent issue and address it properly.

- Measure your results. At the end of the 30 days, look honestly at what changed and what still needs work.

This isn’t a one-time exercise. Businesses that build this kind of review into their regular rhythm tend to catch problems while they’re still small and manageable.

Conclusion

Every successful business faces real challenges – the ones that look effortless from the outside are usually managing the same pressures as everyone else, just earlier and more consistently.

Most business failure isn’t a story of bad luck or an industry that was impossible to crack. It’s a story of preventable mistakes: skipped validation, mismanaged cash, weak planning, and a reluctance to adapt once something stopped working. The encouraging part is that every one of these is something you can actively manage, starting today, regardless of how long you’ve been in business.

If there’s one takeaway worth holding onto, it’s this: focus on continuous improvement rather than chasing quick wins. The businesses that last aren’t the ones that got everything right from day one. They’re the ones that kept paying attention, kept adjusting, and kept showing up for the slow, unglamorous work of building something that holds up over time.

Frequently Asked Questions

What is the biggest reason small businesses fail?

Based on the most current research, a lack of real market demand – building something customers don’t need badly enough to pay for – is consistently cited as the leading root cause. Running out of cash is often the visible symptom that follows.

How can entrepreneurs reduce the risk of business failure?

Validate demand before investing heavily, build disciplined cash flow habits, create a simple but actionable business plan, and stay close enough to customers and competitors that changes in the market don’t catch you off guard.

How important is cash flow management?

It’s one of the most important factors in business survival. A business can have real customers and real revenue and still fail if it doesn’t manage the timing between money coming in and money going out.

Can marketing alone save a struggling business?

Rarely. Marketing can bring in attention and new customers, but if the underlying product, pricing, or cash management is broken, marketing will only accelerate how quickly those problems become visible – not fix them.

What are the early warning signs of business failure?

Declining sales, rising customer complaints, negative cash flow, high employee turnover, low repeat business, and the absence of any measurable goals are the most common signals worth watching closely.